Pay just 0.15% extra and get 1% cash back. Wow – Great deal, No brainer! So you thought!!

Many of us would have heard about cash back scheme on Home Loan Equated Monthly Instalments (EMI) being offered by various banks. Under the cash back scheme, bank would periodically pay back part of the EMI paid as cash back to the customer. In return, all the bank is asking for is slightly higher interest rate. Sounds fair and looks like this is a great deal being offered.

Let’s dig a little deeper.

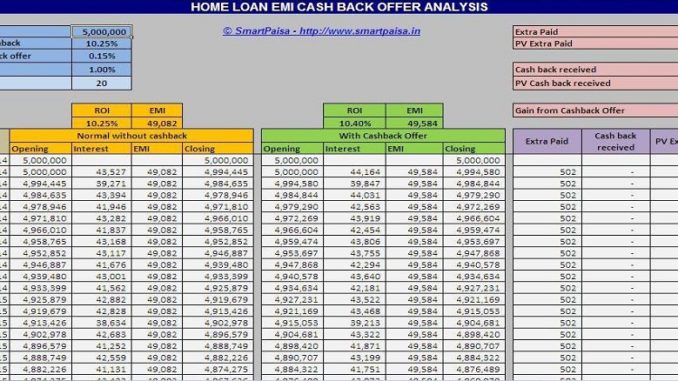

Many banks including ICICI Bank and Axis Bank have in the past introduced some variant of the Home Loan EMI cash back scheme. We have analysed the EMI cash back scheme which was being offered by ICICI Bank. Under the cash back scheme, the bank would offer 1% cash back on the EMIs paid by the customer. First cash back is given, either by way of credit to your bank account or by reduction of principal outstanding of the Home Loan, at the end of 3 years for the total of 36 EMI payments done. Thereafter cash back is given on annual basis for total of 12 EMIs paid in the preceding year. Of course, there are terms which require regular EMI payment to be done by the customer and there being no overdues in order to qualify for cash back, which for the purpose of this analysis, we assume is being fully complied with.

Interest rate on Home Loan availed under cash back scheme is marginally higher (Note typically the bank will offer Home Loan without cash back option also). For instance ICICI Bank is charging a premium of 0.15% on the interest. Thus if the Rate of Interest (ROI) for a normal Home Loan is 10.25%, ROI for Home Loan with cash back offer would be 10.40%. Bank or the Direct Sales Agent (DSA) of the bank would probably make a strong pitch for the offer, explaining just how beneficial the scheme is. Just pay 0.15% interest extra and get whole 1% back.

It would be fallacious to compare 0.15% with 1%. This is the trap most of the people will fall into. Please understand that 0.15% extra interest would be charged on the entire loan amount, while 1% cash back would be refunded on the EMI. Let us try and understand by way of an example.

For a Home Loan of Rs 50 Lakhs for 20 years at ROI of 10.25%, EMI come to Rs 49,082. If cash back offer is availed, applicable interest rate is 10.40% and EMI would go up to Rs 49,584. Thus on a monthly basis, extra outgo on account of higher EMI is Rs 502 per month. Against that cash back amount of 1% of EMI comes to Rs 496 per month. While extra interest is being paid every month, inflow of cash back will be received only on end of 3 years and end of year thereafter. In order to take care of timing difference in the cashflows, we have to calculate the Present Value (PV) of both the cost (extra EMI outgo) and benefit (cash back on EMI). We have used the Home Loan rate of 10.40% as discount rate to compute PV.

Result of Analysis

Cost = PV of extra EMI payment = Rs 50,600

Benefit = PV of cash back = Rs 46,194

Thus on a PV basis there is a loss of Rs 4,406 by availing the cash back offer. The cash back scheme which is being cleverly packaged and marketed as giving overall cash back of approx Rs 1.2 Lakhs on a Rs 50 Lakhs Home Loan, optically looks very appealing but in reality it is a losing proposition.

Please DOWNLOAD the excel model to see detailed calculation. You can play around with variables such as Loan Amount, ROI, extra interest rate for availing cash back offer and cash back rate to analyse various scenarios.

thank you for providing the useful information on home loan and credit car