Mutual Funds Sahi Hai!

You must have heard of this phrase, simple translation of which means Mutual funds are right. Let me add one more adage to your dictionary.

Direct Plans aur bhi Sahi Hai!!

Meaning Direct Plans are even better.

Difference between Regular Plan & Direct Plan

Mutual funds schemes have Regular Plan & Direct Plan. In Regular Plan investment is done through intermediary or mutual fund distributor. Thus when we invest in Mutual Fund through your bank or online trading platform, by default Regular Plan would be subscribed. Whereas, in case you decide to invest directly through the fund house, without involving any intermediary, one can choose Direct Plan.

Underlying portfolio of the scheme, whether you invest in Regular Plan or Direct Plan is exactly same. Difference in the plans lies in the expense ratio, i.e. the charges levied on the fund return. Expense ratio for Regular Plan is higher due to the commission paid by the fund houses to the intermediary or the distributor.

Direct plan of mutual funds can lead to substantial savings in charges over long period of time. Please refer to the expense ratio comparison between Regular & Direct Plans as on July 2017.

| Fund | Regular Plan | Direct Plan | Difference |

|---|---|---|---|

| HDFC Top 200 Fund | 2.10% | 1.35% | 0.75% |

| HDFC Growth Fund | 2.30% | 1.65% | 0.65% |

| HDFC Equity Fund | 2.05% | 1.15% | 0.90% |

| HDFC Mid-Cap Opportunities Fund | 2.23% | 1.23% | 1.00% |

| HDFC Small Cap Fund | 2.46% | 1.31% | 1.15% |

| HDFC Balanced Fund | 1.95% | 0.85% | 1.10% |

| HDFC Prudence Fund | 2.26% | 1.00% | 1.26% |

| Aditya Birla Sun Life Frontline Equity Fund | 2.14% | 0.96% | 1.18% |

| Aditya Birla Sun Life Top 100 Fund | 2.26% | 1.04% | 1.22% |

| Aditya Birla Sun Life Equity Fund | 2.25% | 0.99% | 1.26% |

| Aditya Birla Sun Life Mid Cap Fund | 2.32% | 1.34% | 0.98% |

| Aditya Birla Sun Life Dividend Yield Fund | 2.29% | 1.48% | 0.81% |

| ICICI Prudential Value Discovery Fund | 1.77% | 0.83% | 0.94% |

| ICICI Prudential Focussed Bluechip Fund | 1.78% | 0.81% | 0.97% |

Do not love your financial advisor blindly

What exactly do I mean?

When you buy mutual funds through financial advisor, be it individual or any bank or online brokerage firm (like ICICI Direct or HDFC Securities, etc), investment is done under Regular Plan. This intermediary is paid trail commission every year on the overall amount invested by you. As explained above, this is the incremental expense ratio in regular plans and averages around 1% for equity funds.

Now wait, you will say it is only 1%. It is such a small amount and is justifiable for the convenience or in some cases expert advice rendered. But what if I told you it is really not small amount you are paying for the convenience/ advisory. What if I told you the amount you are paying is over Rs 30 lakhs. Will you still say I love my advisor blindly and am okay to pay this sum?

Rs 30 lakhs loss by investing through Regular Plan

While the difference in expense ratio varies across the fund houses, on an average there is a difference of 1% annual expenses across Regular and Direct Plans. This incremental cost eats into return and can have substantial impact on return over long term.

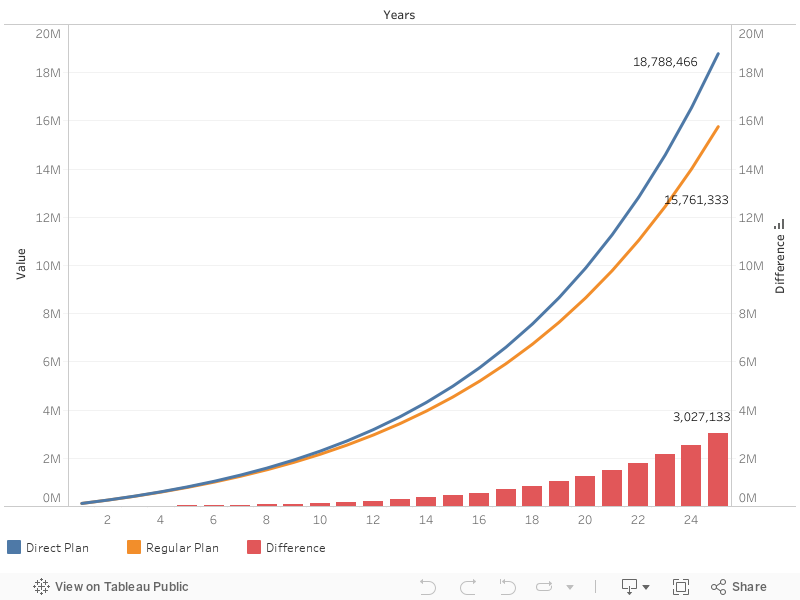

Assuming SIP of Rs.10,000 per month with return in Regular Plan as 11.00% and Direct Plan at 12.00%. We can see from the table below that over the years the difference in return can be a substantial amount.

| Years | Regular Plan | Direct Plan | Difference |

|---|---|---|---|

| 1 | 1,26,239 | 1,26,825 | 586 |

| 2 | 2,67,086 | 2,69,735 | 2,649 |

| 3 | 4,24,231 | 4,30,769 | 6,538 |

| 4 | 5,99,562 | 6,12,226 | 12,665 |

| 5 | 7,95,181 | 8,16,697 | 21,516 |

| 6 | 10,13,437 | 10,47,099 | 33,662 |

| 7 | 12,56,949 | 13,06,723 | 49,773 |

| 8 | 15,28,641 | 15,99,273 | 70,632 |

| 9 | 18,31,772 | 19,28,926 | 97,154 |

| 10 | 21,69,981 | 23,00,387 | 1,30,406 |

| 11 | 25,47,328 | 27,18,959 | 1,71,631 |

| 12 | 29,68,340 | 31,90,616 | 2,22,275 |

| 13 | 34,38,072 | 37,22,091 | 2,84,019 |

| 14 | 39,62,160 | 43,20,970 | 3,58,809 |

| 15 | 45,46,896 | 49,95,802 | 4,48,906 |

| 16 | 51,99,296 | 57,56,220 | 5,56,924 |

| 17 | 59,27,191 | 66,13,078 | 6,85,886 |

| 18 | 67,39,318 | 75,78,606 | 8,39,289 |

| 19 | 76,45,422 | 86,66,588 | 10,21,166 |

| 20 | 86,56,380 | 98,92,554 | 12,36,173 |

| 21 | 97,84,325 | 1,12,74,002 | 14,89,677 |

| 22 | 1,10,42,795 | 1,28,30,653 | 17,87,858 |

| 23 | 1,24,46,893 | 1,45,84,726 | 21,37,833 |

| 24 | 1,40,13,472 | 1,65,61,259 | 25,47,787 |

| 25 | 1,57,61,333 | 1,87,88,466 | 30,27,133 |

Thus over 25 year period, mere 1% difference in expense ratio can lead to difference in investment value of upto INR 30.27 lakhs.

Thus clearly Direct Plans of Mutual Funds scores high in comparison to the Regular Plan. But is there still case for Regular Plan? Lot of literature would be available on the internet propagating the Regular Plans due to advantage of advisory service being offered by the financial advisors. But quite frankly most of the proponents of Regular Plans have a vested interest in terms of pushing Regular Plan. In terms of selection of proper funds, enough material is freely available which can enable proper selection of funds. Thus overall it makes immense sense to choose Direct Plans over Regular Plan of Mutual Funds.

Leave a Reply